Intro

In recent years rare-earth elements have received increasing attention worldwide, and many countries have included them in the list of key metallic minerals. The US Department of Energy calls them “technological metals”. Thus, rare and rare-earth metals have become strategic resources for which the world’s largest economies compete.

World industry rapid shifting to electric vehicles and «green» technologies requires titanium, molybdenum, zinc, lithium, cobalt and other metals.

Currently, about 300 minerals containing rare-earth elements are known.

Where rare and rare-earth metals are found in nature.

The main minerals that contain rare-earth elements are: bastnasite, monazit sand, loparite, lateritton, xenotime, pyrochlore, fergusonite, samarskite and others.

Other minerals that are used as a source of rare-earth elements include apatite, euxenite, gadolinite. Allanite, fluorite, perovskite and zircon may be future sources of rare earth elements.

The content of individual rare-earth elements varies greatly from mineral to mineral and from deposit to deposit.

Most of the resources of rare-earth elements are concentrated in bastnasite deposits in China and the USA, and monazite deposits – in Australia, Brazil, China, India, Malaysia, South Africa, Sri Lanka, Thailand and the USA.

The most important rare-earth mineral is bastnasite, which is present in significant quantities in the ores of the Mountain Pass (California), Bayan Obo (China), Wugu Hill (Tanzania), Karonge (Burundi) deposits.

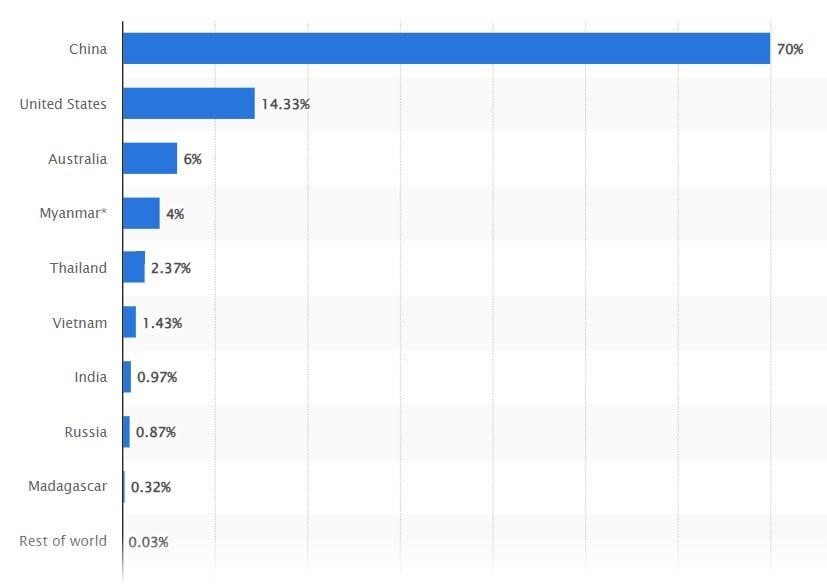

In terms of world reserves of rare-earth minerals China ranks first, Vietnam – second, Brazil – third. India, Australia, Russia, the USA and Canada have rich resources of rare-earth elements. In recent years large deposits of rare-earth elements have also been discovered in South Africa, Malaysia, Indonesia and other countries.

Data on REE reserves are presented in the diagram.

Deposits of rare-earth elements in different countries of the world.

Projects for development of deposits of rare-earth elements have been announced in a number of countries. However, previously many of these initiatives failed due to high costs and the presence of relatively cheap Chinese products on the market.

In northern Sweden, near the city of Kiruna, a large deposit of rare-earth metals was discovered, which is most likely the largest known in Europe. The LKAB Mining company reported that deposits had been found near one of its operating mines; there can be about a million tons of raw materials. According to the company: «This is the largest known deposit of rare-earth elements in our part of the world and could significantly contribute to getting raw material, neede to the «green transition».

In 2011 a group of Japanese researchers discovered rare-earth ore deposits at the bottom of the Pacific Ocean by analyzing soil samples from 80 wells with the depth of 3.5 to 6 km. The ore deposit extends from the Minami-Torishima Islands into international waters west and east of Hawaii and east of Tahiti. The predicted ore resources of these deposits are estimated at 80-100 billion tons. According to Japanese researchers, the ores of the underwater deposit are 20-30 times richer in rare-earths than Chinese deposits. As the scientists report, this deposit contains reserves of yttrium, which will last for the humanity for 780 years, europium for 620 and terbium for 420 years.

Norwegian authorities are finalizing a plan of mining a range of metals from the bottom of the Greenland and Norwegian seas southwest of Svalbard to help Europe meet its urgent need for rare-earth elements. Norway may become the first country to extract such metals from the seabed.

According to information of the British company SRE Minerals, the world’s largest rare earth-metal deposit was discovered in DPRK, in the south of North Pyongyang province. Its reserves are tentatively estimated at 6 billion tons of ore, which contains 216 million tons of rare-earth oxides – mostly light and about 2.66% – the most valuable heavy lanthanoids.

Currently, mining companies in China, Japan, New Zealand, and Papua New Guinea are exploring the ways to extract rare-earth metals from their territorial waters.

Development of new deposits is a matter of many years and even decades, so dependence on China in supplying the world economy with rare-earth metals will not disappear in the near future.

World production of rare-earth elements.

Production of rare-earth elements in different countries of the world.

Until the early 1990s the main producer of rare-earth elements were the United States (Mountain Pass deposit).

In 1986 the world produced 36 500 tons of rare-earth metal oxides. 17 000 tons of them were produced in the USA, 8 500 tons – in the USSR, 6 000 tons – China.

In the 1990s the industry was modernized in China with participation of the state, when the directive idea of Deng Xiaoping began to be implemented: «Rare metals are the same for China as oil is for Arab countries».

Since the mid-1990s China has become the largest producer of rare-earth elements, extracting up to 120 thousand tons at the Bayan Obo deposit, owned by the Inner Mongolia Baotou Steel Rare-Earth state company.

More than 200 large and small enterprises for extraction and processing of rare-earth elements operated on its territory. China and surrounding countries have become the main producers of electronic products. All major global companies purchased REE raw materials from China. And not only because of the cost of these raw materials, but also due to tha fact that it is an extremely environmentally harmful production.

In the 2010s China implemented a policy of limiting production and export of rare-earth metals, which stimulated higher prices and increased production in other countries. World analysts explained such actions by many reasons: from an attempt to completely take control of the global production of high-tech products to the depletion of two-thirds of Chinese deposits. In 2015, China re-opened the market, but the world had already learned the lesson taught by the monopolist. Since deposits of rare-earth elements in the world are not so rare, countries with their reserves have begun to pay attention to their local deposits.

The main producers of REE in the world market are the USA and China, besides them – Australia, Malaysia, Brazil and other countries. Thailand and Vietnam are also increasing production.

The Vietnamese government intends to increase development of rare-earth ores to 2 million tons per year by 2030, reports Reuters. According to the US Geological Survey (USGS), Vietnam’s REM reserves (about 22 million tons) are the second largest in the world after China. Production is growing rapidly: from 400 tons in 2021 to 4300 tons in 2022.

China is a leader in production of rare-earth metals.

China is currently accounted for by about 70% of the world’s rare-earth metal concentrate production and 90% of the finished product. At the moment this country is the only one that has a complete production chain of rare-earth metals – from mining and processing to delivery to customers. Due to problems with the USA prices for these metals continue to rise constantly.

More than half of the rare-earth production in China is concentrated in the «Rare Earth Valley» near the city of Baotu on an area of 50 km2. The Chinese government is investing much in creating a global cluster center for the rare-earth industry in the region.

In July 2023 China announced that it would impose restrictions on export of gallium and germanium, essential metals for manufacturing strategic products such as electric vehicles, microchips and some weapons.

Rare-earth metals are a powerful tool of Chinese foreign policy, the main mean for attracting innovative technologies into the country.

Western governments are desperate to catch up with China in producing critical minerals and securing the supply chain for «green energy» equipment. Billions of dollars are being allocated for this. Analysts did not come to an agreement on how long it will take the West to do away from its dependence on China in this issue, or whether it is even possible.

BYD, the Chinese electric vehicle producer, now poses an existential threat to traditional automobile manufacturers in Germany, France, the USA and Japan, but once it was a money-losing state-owned company.

Goldman data show that China could build an electric vehicle factory three times faster that other countries. Besides, a battery plant in the USA will cost almost 80% more than in China. It is not just the issue of access to resources or high costs, the West has problems with shortage of manpower and inflation but also with higher environmental standards.

The situation is the same with solar and wind energy equipment. Mining and processing polysilicon costs a third less in China than in Europe. S&P reports that Chinese wind turbines cost twice less than the Western ones.

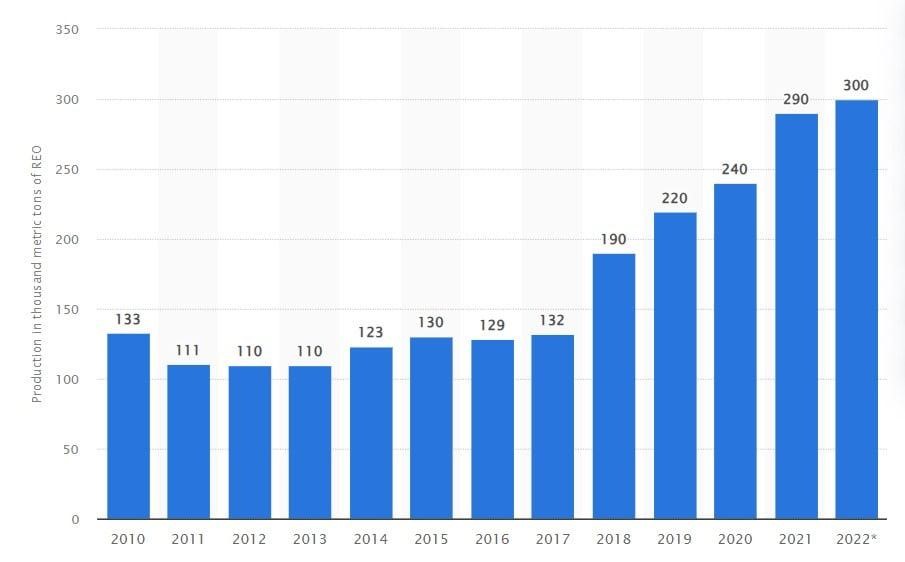

World production of rare-earth metals and market development trends in different countries.

Distribution of production of rare-earth metals in the world (in%) as of 2022 can be seen in the diagram.

Production of rare-earth metals in the world in the period from 2010 to 2022 in thousand tons is presented in the diagram.

Indian authorities plan to ban the export of four important metals – lithium, beryllium, niobium and tantalum – as a strategy to ensure India’s self-sufficiency in critical metals and minerals. The above metals are crucial for the Indian energy, aerospace and defense sectors and are important for national security and technological progress.

Simultaneously with the development of legal mining, a gray and black market of rare-earth elements appeared in the world. Experts find it difficult to determine their volumes. Most probably these elements come to third world countries, where counterfeits of world brands are produced in clandestine workshops.

Recycling of products, containing rare-earth elements, is usually difficult, so its volume is extremely small. Only magnetic alloys are actually recycled and reused.

According to experts, in the future, by 2050, the demand for rare-earth metals may increase by at least ten, or even several dozen times. Therefore, a strategy for obtaining these critical raw materials is required, including their extraction from the devices in which they have been used.

Today the development of the raw material base of rare-earth metals as well as their production is hampered by two problems: the high cost of extraction and the expensive and labor-intensive process of separating elements. The world’s leading universities and scientific departments of manufacturing companies are working on solving these problems.

It is necessary to solve numerous scientific and technical issues. Firstly it is needed to create consumer products that can be easily recycled at the end of their service life, and secondly – recycling of rare-earth elements should be economical, and, therefore, the use of extremely valuable but limited nature resource optimal.

CONCLUSION

Currently, about 300 minerals are known that contain rare-earth elements.

In terms of world reserves of rare-earth minerals China ranks first, Vietnam – second, Brazil – third. India, Australia, Russia, the USA and Canada have rich rare-earth resources.

Projects for development of deposits of rare-earth elements have been announced in a number of countries, but this development is hampered by high costs, environmental restrictions and the presence of relatively cheap Chinese products on the market.

Until the early 1990s, the United States was the main producer of rare-earth elements.

Since the mid of the 1990s China has become the largest producer of rare-earth elements. Currently China is accounted for by about 70% of the world’s rare-earth metal concentrate production and 90% of the finished product.

In addition to China, the main producers of REE on the world market are the USA, Australia, Malaysia, Brazil and other countries. Thailand and Vietnam are increasing production.

According to experts, in the future, by 2050, the demand for rare-earth metals may increase by at least ten, or even several dozen times.

Today, the development of the raw material base of rare-earth metals as well as their production, is hampered by two problems: the high cost of extraction and the expensive and labor-intensive process of separating elements.